On the verge of amazing growth in solar and batteries – but still far behind 2°C trajectory

More PV panels are being mounted – but still more are needed.

Dette er et debattinnlegg. Teksten er kvalitetssikret i tråd med redaksjonelle prinsipper for publisering. Innholdet reflekterer skribentens egne meninger.

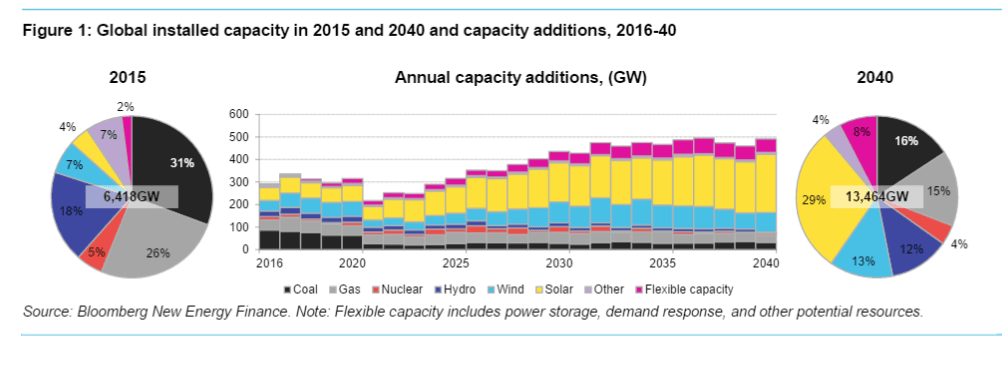

"New Energy Outlook 2016" (NEO 2016), the yearly flagship publication from Bloomberg’s 65 new energy experts from around the world published mid-June, is fascinating reading. Despite cheaper coal and cheaper gas, wind and solar are now the leading sources of new generation capacity added worldwide. By 2040, hydro, wind, solar and batteries will make up 60% of installed capacity, projects Bloomberg New Energy Finance. Wind and solar will account for 64% of the 8.6TW of new power generating capacity added worldwide over the next 25 years.

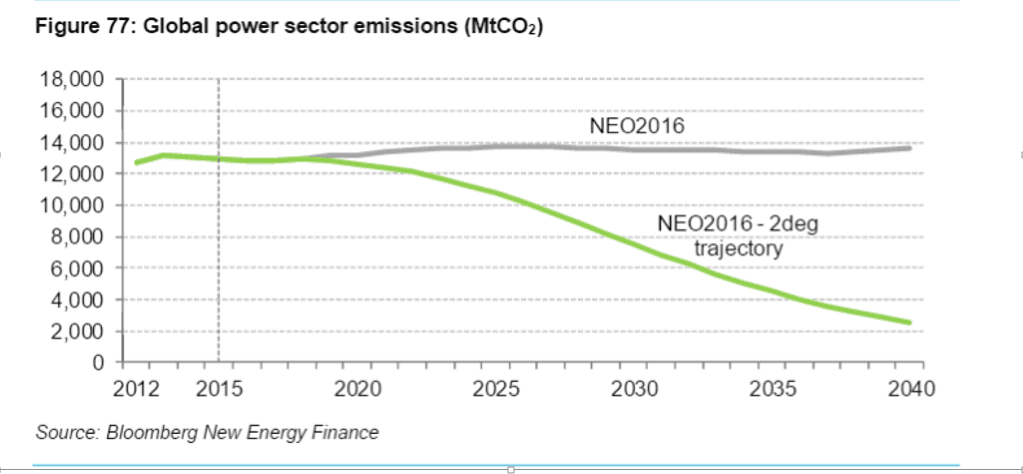

This strong growth, says Bloomberg, will be driven mainly by economics. In fact, most countries will have phased out subsidies to renewable energy by 2020. But impressive as it is, this projected colossal growth in renewables is still far from sufficient to what’s required to meet the 2°C trajectory. A 50 % additional increase in green energy investments will be needed.

The main driving force behind the growth is wind and in particular solar keep getting cheaper. By 2030, solar power will have emerged as the cheapest generation technology in most countries. By around 2027, Bloomberg estimates it will even be more economic to build new wind and solar than running existing coal and gas generators, particularly where carbon pricing is in place. Another factor reinforcing decarbonisation is electrification of the transport sector, mainly driven by continuous decline in cost of batteries. NEO 2016 projects electric vehicles will make up 25% of the global car fleet by 2040.

It is also interesting to note that natural gas, in Bloomberg’s analysis, does not succeed to become a key 'transitional fuel’ between coal and renewables. In fact, natural gas’ share of the world total installed generation capacity drops from 26 to 16 % between 2015 and 2040. Its share of total global generation, however, increases from 9 to 16 %. This is because natural gas plants have higher capacity factors than the intermittent sources wind and solar. But despite the higher capacity factor, Bloomberg projects that by 2040 the world’s solar plants will generate 100 % more electricity than all the world’s natural gas plants.