On the verge of amazing growth in solar and batteries – but still far behind 2°C trajectory

More PV panels are being mounted – but still more are needed.

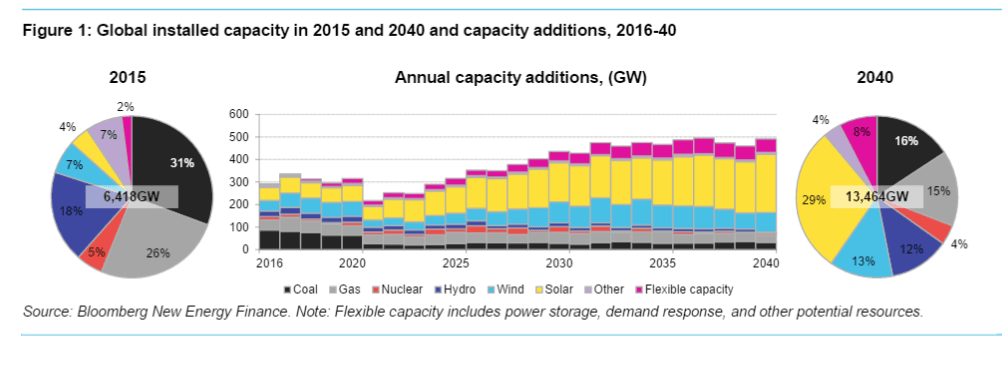

"New Energy Outlook 2016" (NEO 2016), the yearly flagship publication from Bloomberg’s 65 new energy experts from around the world published mid-June, is fascinating reading. Despite cheaper coal and cheaper gas, wind and solar are now the leading sources of new generation capacity added worldwide. By 2040, hydro, wind, solar and batteries will make up 60% of installed capacity, projects Bloomberg New Energy Finance. Wind and solar will account for 64% of the 8.6TW of new power generating capacity added worldwide over the next 25 years.

This strong growth, says Bloomberg, will be driven mainly by economics. In fact, most countries will have phased out subsidies to renewable energy by 2020. But impressive as it is, this projected colossal growth in renewables is still far from sufficient to what’s required to meet the 2°C trajectory. A 50 % additional increase in green energy investments will be needed.

The main driving force behind the growth is wind and in particular solar keep getting cheaper. By 2030, solar power will have emerged as the cheapest generation technology in most countries. By around 2027, Bloomberg estimates it will even be more economic to build new wind and solar than running existing coal and gas generators, particularly where carbon pricing is in place. Another factor reinforcing decarbonisation is electrification of the transport sector, mainly driven by continuous decline in cost of batteries. NEO 2016 projects electric vehicles will make up 25% of the global car fleet by 2040.

It is also interesting to note that natural gas, in Bloomberg’s analysis, does not succeed to become a key 'transitional fuel’ between coal and renewables. In fact, natural gas’ share of the world total installed generation capacity drops from 26 to 16 % between 2015 and 2040. Its share of total global generation, however, increases from 9 to 16 %. This is because natural gas plants have higher capacity factors than the intermittent sources wind and solar. But despite the higher capacity factor, Bloomberg projects that by 2040 the world’s solar plants will generate 100 % more electricity than all the world’s natural gas plants.

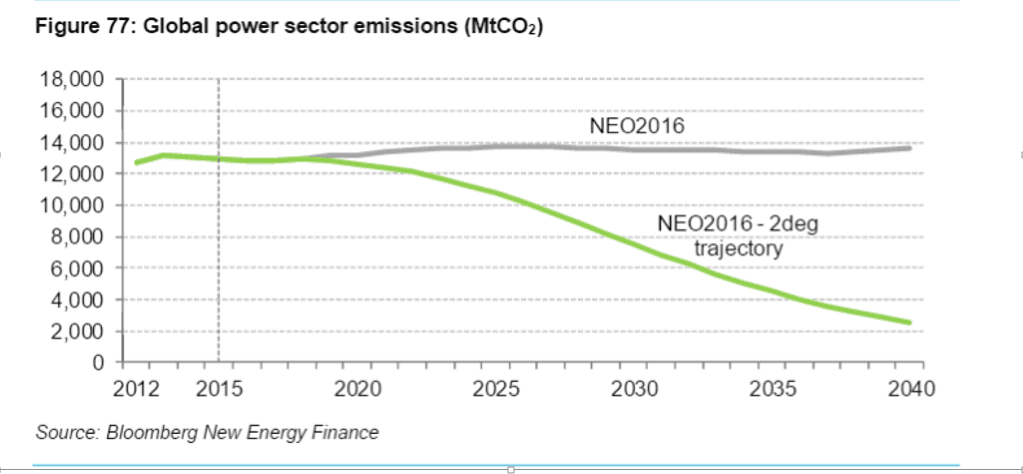

The main message to be read from Bloomberg’s latest report, however, is a more sober one. As the energy sector make up two-thirds of global greenhouse gas emissions, the target to stabilize and reduce carbon emissions will require a deep decarbonisation of the power systems. By 2040, Bloomberg expects the energy intensity of the world economy to fall by 28% and its carbon intensity by 50%. China will see the greatest reduction of both carbon and electricity intensity in absolute terms.

But despite this significant progress, we’re still far behind what is needed to meet the 2°C trajectory, warns Bloomberg. If we want to follow the trajectory leading to 50 % chance of keeping the global warming below 2°C, Bloomberg estimates that "around 10TW of zero-carbon power generation will need to be installed by 2040, representing a $14.6 trillion investment opportunity over the next 25 years". This is 56% more new capacity than under the NEO 2016 forecast which anticipates the need for $9.3 trillion of new zero-carbon investment, or around $373 billion per year. This means that yearly investments in zero-carbon technologies must increase from about 373 billion in Bloomberg’s "un-subsidized" scenario, to about 560 billion average per year in a climate-resilient scenario.

190 billion USD yearly in "additional" investments is a huge amount, but the costs of postponing these investments are much higher. Fortunately, the private sector is ready to develop and finance the required accelerated investments in renewables, storage, etc. What governments need to assure, through the new Green Climate Fund or finance institutions already involved in green energy financing, is the availability of guarantees, low-interest loans or other instruments that will make clean energy an attractive alternative when competing against new coal-fired plants in Asia and Africa. "New Energy Outlook 2016" is a timely reminder of the need to move forward on the pledge in Paris to allocate 100 Billion USD yearly in new climate finance to the developing countries, where most of these investments will need to take place.